Executive Summary

The Midwestern United States1 is called “the Heartland” for a reason. The region is our nation’s center for commodity agriculture, manufacturing, and transportation logistics. It’s also home to vibrant cities, dense forests, and countless tributaries and lakes. All told, it is one of the most economically productive regions of America.

But climate change puts that productivity at risk. While this is an area accustomed to dramatic weather events, the extremes that are likely to come with climate change are on an entirely different scale for the region’s businesses, communities, and overall economic health.

Rising heat resulting from increased greenhouse gas emissions is likely to affect the Midwest region’s ten major metropolitan areas through higher heat-related mortality, increased electricity demand and energy costs, and declines in labor productivity. Meanwhile, without significant adaptation on the part of Midwest farmers, the region’s thriving agricultural sector—particularly in the southern states—is likely to suffer yield losses and economic damages as temperatures rise.

In addition, potential changes in the intensity, form, and timing of precipitation in the region—including snowfall, rain, and evaporation off the Great Lakes and Mississippi River—will pose challenges for regional infrastructure managers, farmers, and businesses.

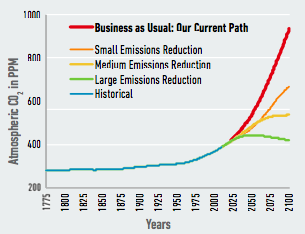

The mission of the Risky Business Project is to quantify the economic risks to the U.S. from unmitigated climate change. Our inaugural report, Risky Business: The Economic Risks of Climate Change in the United States,2 highlighted these risks across every region of the country, with a focus on three sectors: agriculture, energy demand, and coastal infrastructure. We also looked at overarching issues such as changes in labor productivity, heat-related mortality, and crime. This follow-up report, Heat in the Heartland: Climate Change and Economic Risk in the Midwest, zeros in on the Midwest and offers a first step toward defining the range of potential economic consequences to this particular region if we continue on our current greenhouse gas emissions pathway.3

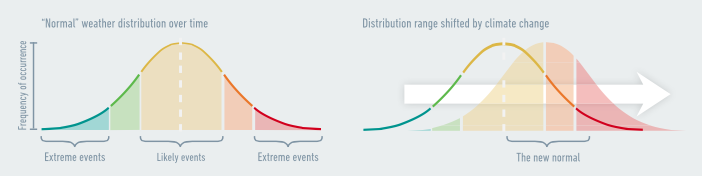

Our research combines state-of-the-art climate science projections through the year 2100 (and beyond in some cases) with empirically-derived estimates of the impact of projected changes in temperature and precipitation on the Midwest economy. We analyze not only those outcomes most likely to occur, but also lower-probability, higher-cost climate futures. These are the “tail risks,” most often expressed here as the 1-in-20 chance something will occur. Unlike any other study to date, we look at climate impacts at a very geographically granular level, in some cases providing county-level results.

Our findings show that if we stay on our current emissions path, the Midwest will likely experience significant economic impacts from climate change. These changes are both negative and positive, varying greatly from the southern to the northern parts of the region. However, if the region chooses a different path—if state and regional policymakers and business leaders act aggressively to adapt to the changing climate and also to mitigate future impacts by reducing their own carbon emissions—the Midwest can demonstrate to our national and global political leaders the kind of strong response that is necessary to reduce the worst future economic risks from climate change.

Heat in the Heartland—Extreme Heat Likely to Hit Midwest Agriculture, Manufacturing, and Cities

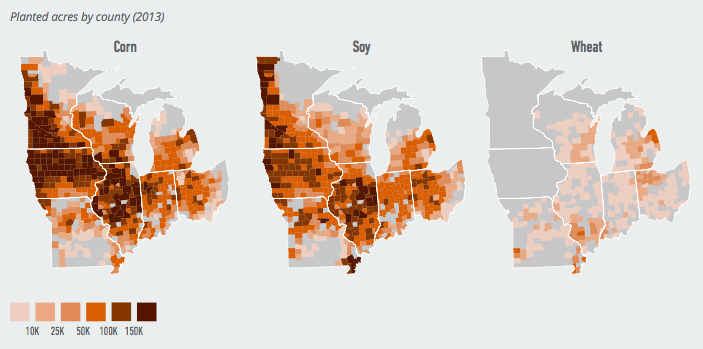

As a region, the Midwest is home to nearly one in five Americans and includes many of the nation’s most populous cities, including Chicago, Minneapolis-St. Paul, Indianapolis, Columbus, Detroit, Milwaukee, Kansas City, Cleveland, and St. Louis. The region is also known for both agriculture and energy-intensive manufacturing: The Midwest is responsible for 65% of U.S. production of corn and soybeans,4 a significant share of the national wheat crop, and about a third of all U.S. manufacturing operations.5

Without action, climate change will lock in extreme temperature increases across the Midwest, bringing severe risks to the southern states’ economies, and potentially some moderate temperature and agricultural benefits to states in the northern part of the region. These risks include:

- By the end of this century, dangerous levels of extreme heat are likely across the southern Midwest.

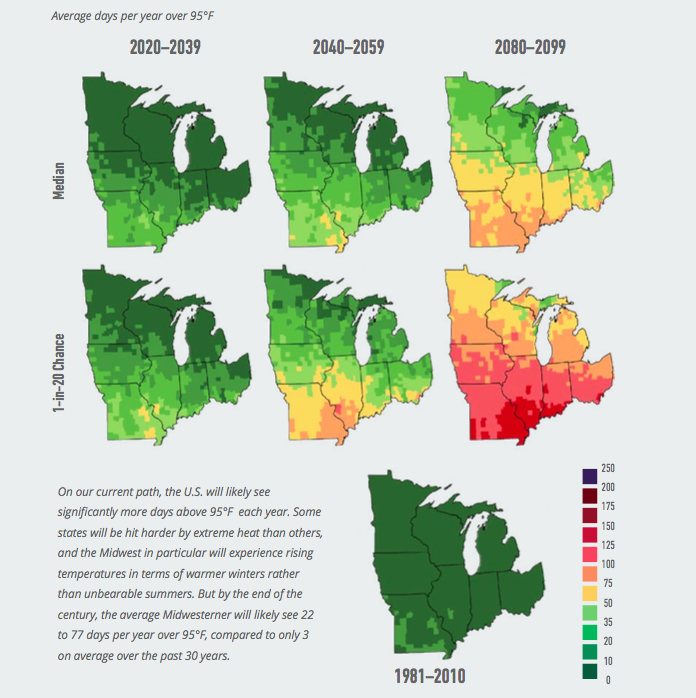

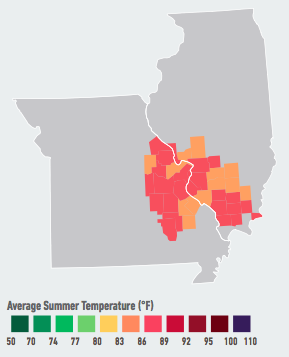

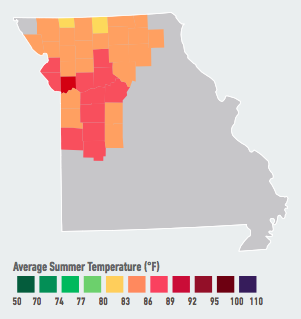

- By the end of this century, the average Missouri resident will likely experience 46 to 115 days above 95°F in a typical year—about as many extremely hot days as the average Arizonan has experienced each year in recent decades. There is a 1-in-20 chance that Missouri will experience more than 125 such days by the end of the century.

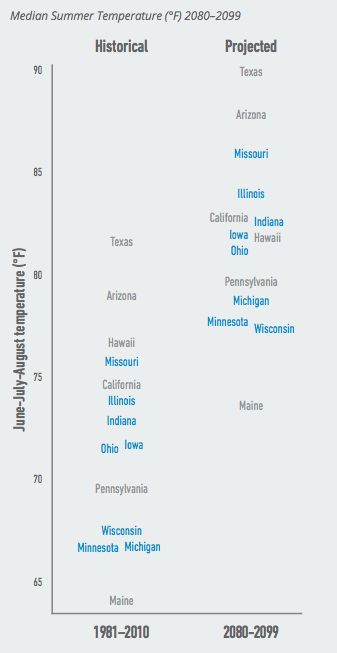

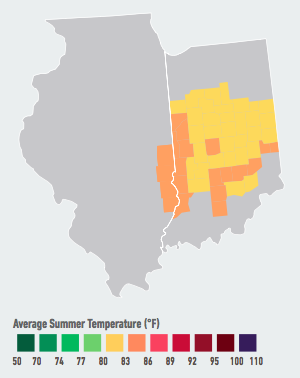

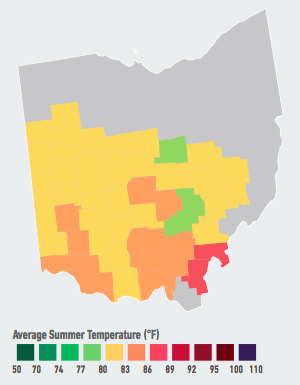

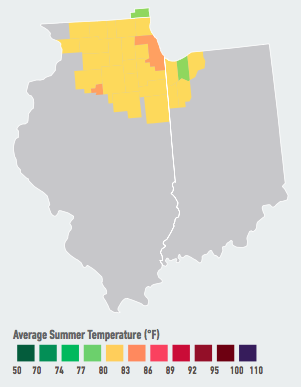

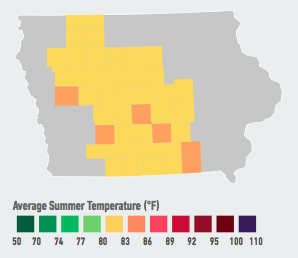

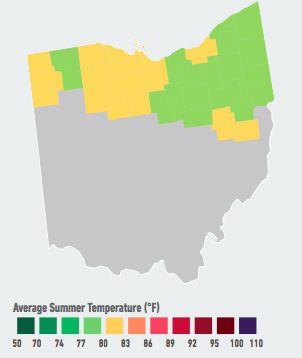

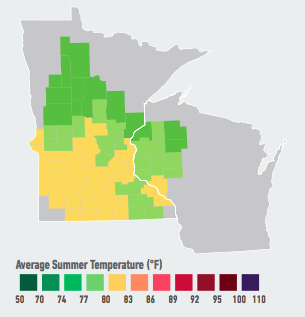

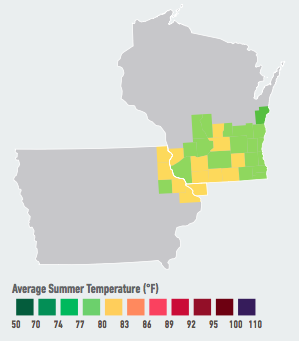

- Summer average temperatures in Minnesota, Wisconsin, and Ohio are expected to be hotter by century’s end than average summer temperatures in Washington, D.C., today.

- The average Chicago resident is expected to experience more days over 95°F each year by century’s end than the average Texan does today, with a 1-in-20 chance that these extremely hot days will be more than double Texas’s average.

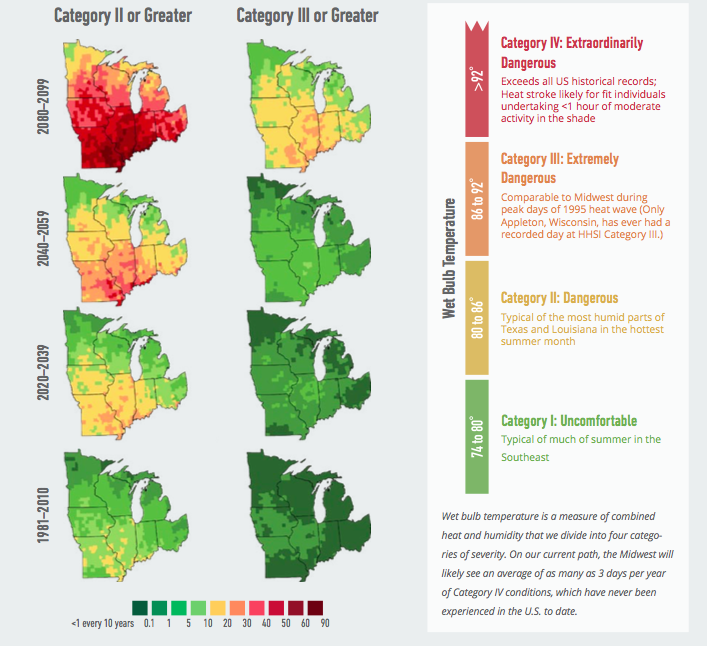

- Rising humidity combined with increased heat across the region will likely mean more frequent days that reach extremes on the “Humid Heat Stroke Index.”6 There is a 1-in-20 chance that the city of Chicago will experience more than 10 days per year by the middle of this century with heat and humidity conditions similar to the heat wave of 1995, which caused approximately 750 deaths.

- Northern Midwest states may see fewer deaths as winters warm—but also fewer fish, and less winter recreation.

- By the end of this century, only two upper Midwest states (Minnesota and Wisconsin) are expected to have average winter temperatures below the freezing mark.

- By mid-century, the average Midwesterner will likely experience 16 to 37 fewer days below freezing each year (with a 1-in-20 chance of more than 52 fewer days); by the end of the century, there will likely be 40 to 72 fewer days below freezing (with a 1-in-20 chance of more than 88 fewer days).

- Fewer freezing days translates into less energy used for heating and fewer cold-related deaths; however, warmer winters will also lead to decreased snow and ice for outdoor winter sports like hockey, snowmobiling, and ice-fishing. These winter tourism industries employ over 35,000 workers in the Midwest region.7

- As streams and lakes become warmer, fish and other sensitive water-based species may be threatened.8

- By the end of this century, only two upper Midwest states (Minnesota and Wisconsin) are expected to have average winter temperatures below the freezing mark.

Figure 1. Average Days Over 95°F: A Departure from the Norm. Data Source: American Climate Prospectus.

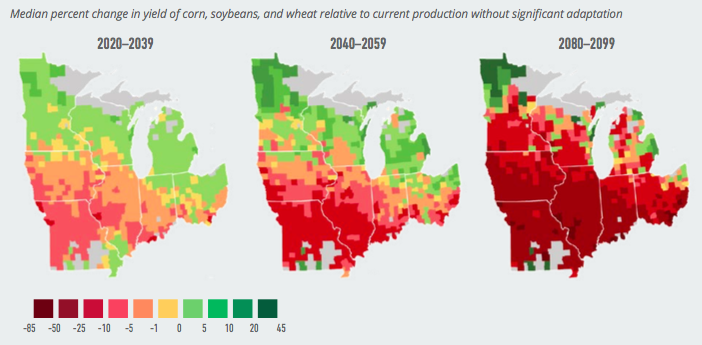

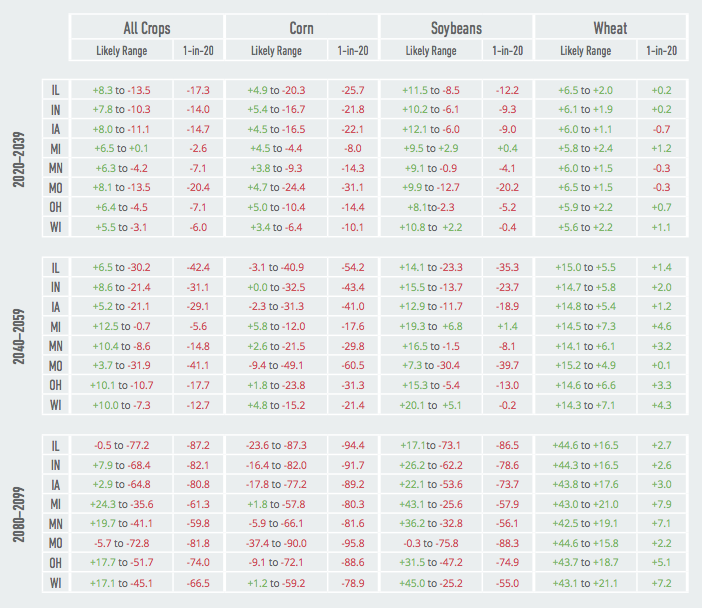

- Changes in temperature and precipitation will shift agricultural patterns and affect crop yields, with gains in certain crops offset by losses in others.

- Over the next 5 to 25 years, without significant adaptation by farmers, some counties in Missouri, Illinois, and Indiana will likely see average commodity crop losses up to 18 to 24% due extreme heat each year.

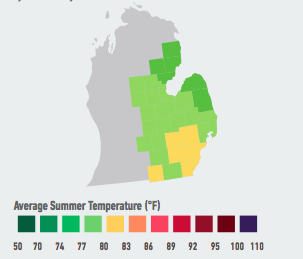

- On the other hand, warmer winters may extend growing seasons in Minnesota, Wisconsin, and Michigan, allowing farmers to practice double-cropping.

- If we continue on our current emissions path without significant adaptation, by the end of the century the Midwest will likely see overall agricultural losses for corn and wheat of 11% to 69% across the region as a whole, with a 1-in-20 chance of more than an 80% decline.

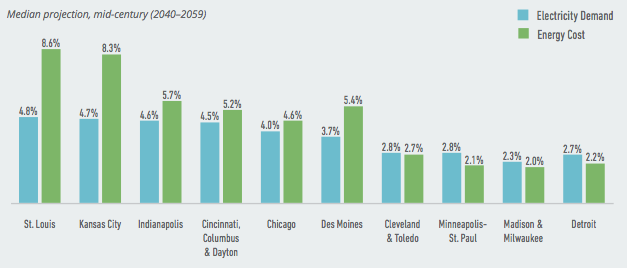

- Increased heat will raise electricity demand while decreasing energy system capacity, leading to higher energy costs particularly in the manufacturing-intensive southern states.

- The Midwest region is energy- and emission-intensive, due to the prevalence of energy-intensive manufacturing, substantial dependence on coal-fired power, and emissions from mining and agriculture. As a result, energy use per dollar of GDP in this region is more than 20% higher than the national average, and per capita greenhouse gas emissions are 22% above the national average.9

- Electricity demand will grow as households and businesses increase their use of air conditioning in response to temperature increases throughout the region. The Midwest in particular will see large energy cost increases due to expenditures associated with switching from heating demand to cooling demand. For instance, the most southern Midwest state of Missouri will likely see a 4% to 16% jump in energy costs by mid-century, with a 1-in-20 chance this jump will be more than 20% by mid-century.

- Precipitation will likely become more extreme. While it’s difficult to predict future rain and snowfall, climate change is likely to increase the incidence of extreme rainfall events across the Midwest, leading to flooding and related property and crop losses.

- The timing of rainfall across this region may also shift, affecting growing seasons for farmers and putting additional strain on already-taxed stormwater management and wastewater treatment infrastructure.

- Rising temperatures will reduce labor productivity while increasing crime rates and heat-related mortality.

- When heat rises past human comfort levels, labor productivity declines, particularly in “high-risk” industries involving outdoor work (these include construction, transportation, agriculture, and manufacturing).

- By the end of the century, the St. Louis, Missouri, metro area will likely see labor productivity declines of as much as 3.3% in these high-risk industries, which is comparable to the decline in absolute labor output during past U.S. recessions.10 In St. Louis, there is a 1-in-20 chance of declines in labor productivity of more than 4.6% by end of century.

- Rising heat will likely cause increased heat-related mortality in the southern states. For example, the Kansas City metro area will likely experience as many as 24 likely additional deaths per 100,000 residents by the end of the century, with a 1-in-20 chance of more than 36 additional deaths per 100,000 residents.

- Rising heat is also one factor in higher violent crime rates, with as much as a 6.4% increase in crime likely (and a 1-in-20 chance of more than a 8.1% increase) in the Minneapolis-St. Paul metro area by the end of the century.

- At the same time, northern states will likely benefit from reduced cold-related mortality.

{kind=link}