Addressing climate risk requires a transition to an economy powered by clean energy. Our research leads to the following general findings:

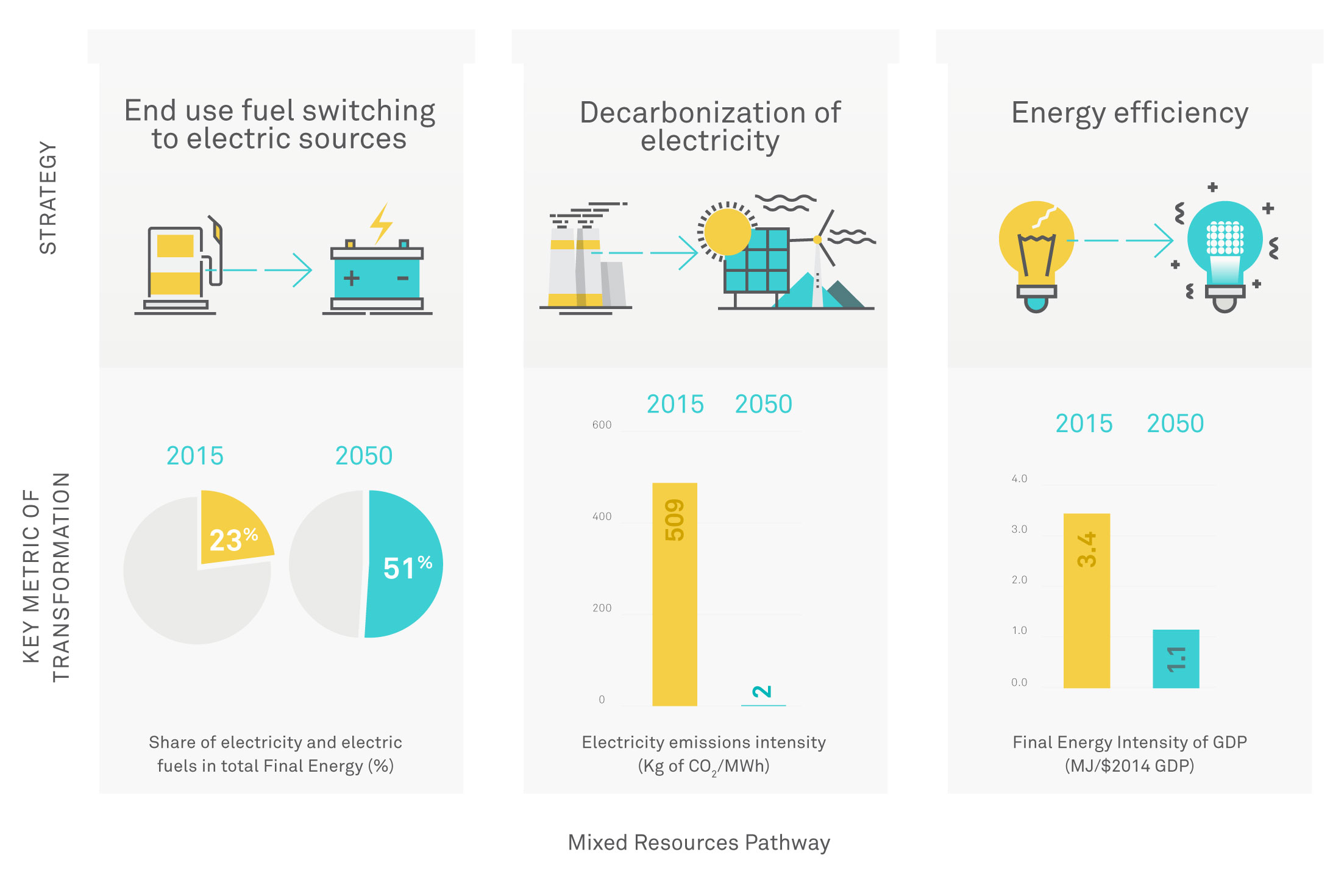

- Shifting to a cleaner energy economy requires three major changes: switching from fossil fuels to electricity wherever possible; generating electricity with low or zero carbon emissions; and using energy more efficiently.

- These changes involve substantial capital investments up front, but these investments will be offset by fuel savings. Essentially, the shift substitutes up-front capital investment for long-term fuel spending.

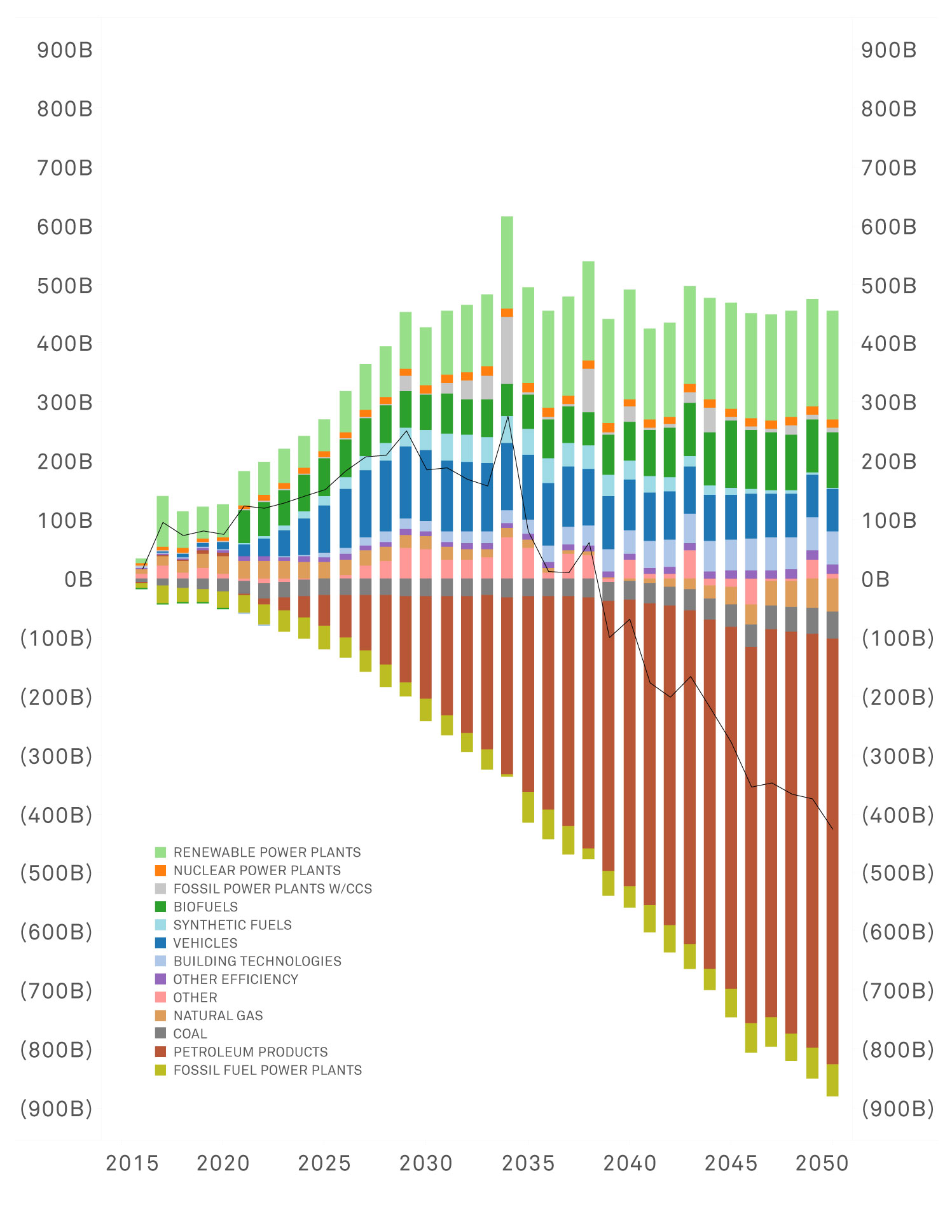

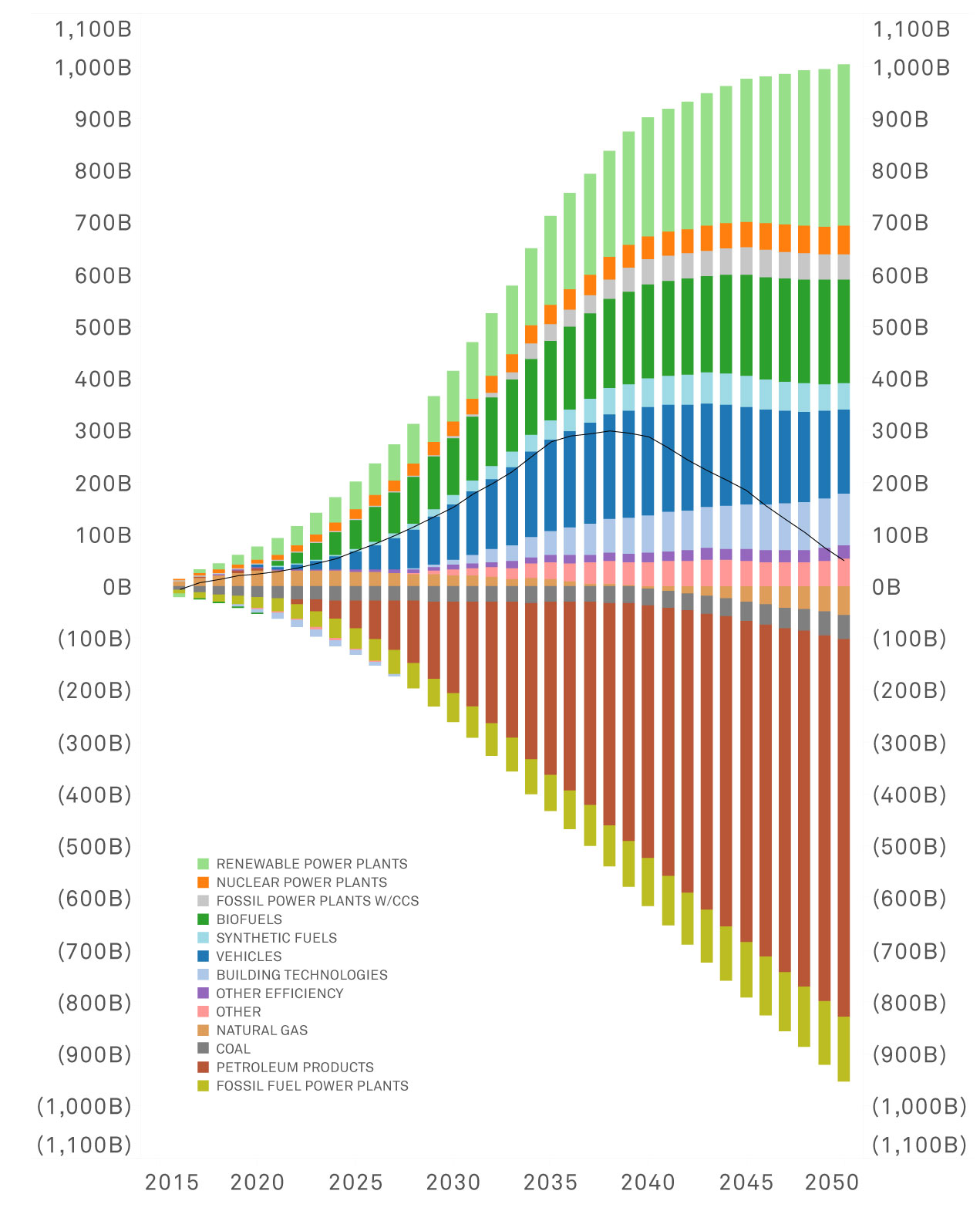

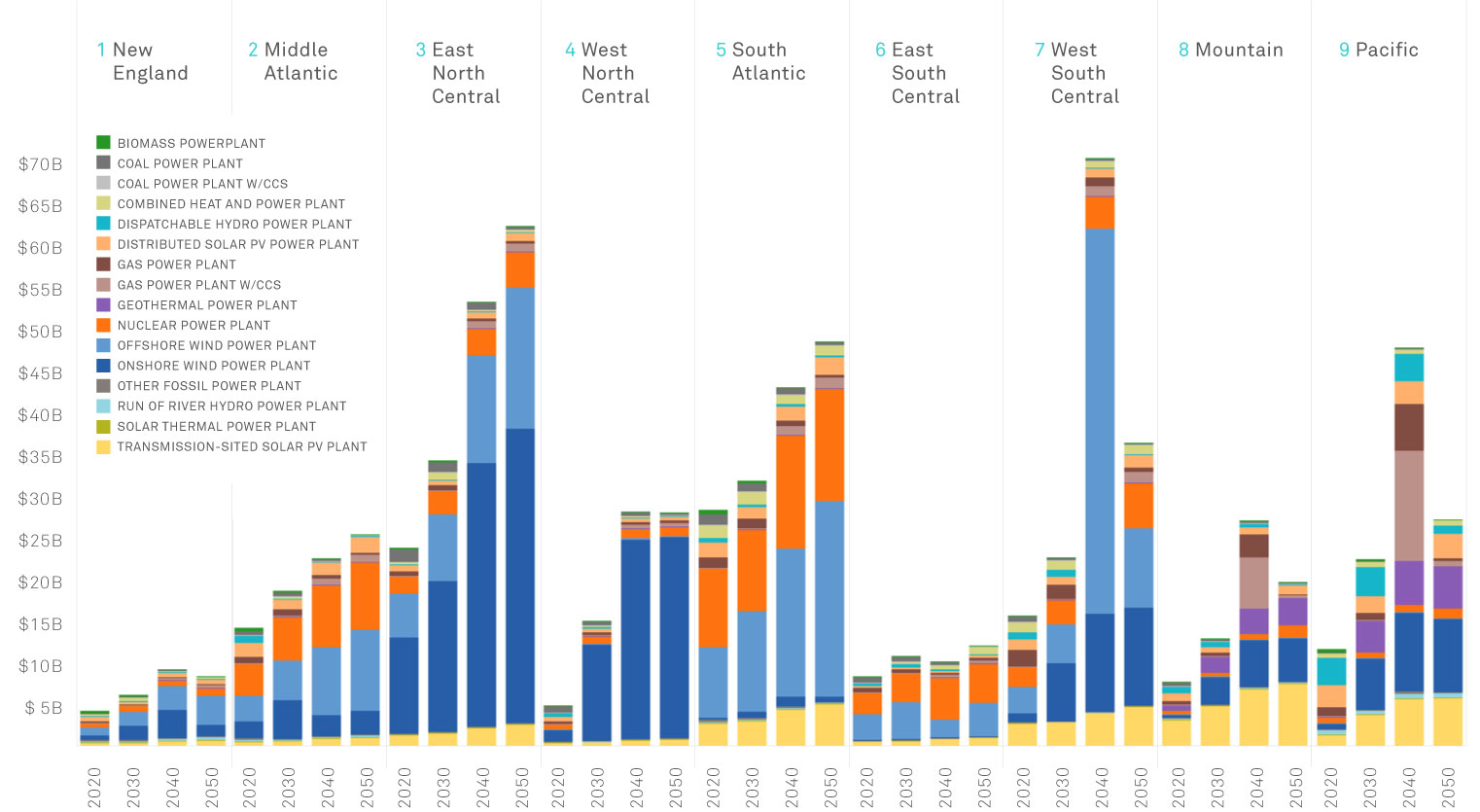

- The largest increases in investment in the 2020-2030 period would be in vehicles of all types ($75 billion per year); power generation ($55 billion per year); advanced biofuels such as renewable diesel ($45 billion per year); and energy efficiency measures ($16 billion per year). The total additional capital investment would average about $200 billion per year from 2020 to 2030, and then average about $400 billion per year between 2030 and 2050. (Results are for the Mixed Resources pathway, one of four modeled.)

- The investment needed to transition to a clean energy economy is likely less than either the economic costs of unmitigated climate change or the projected spending if the U.S. continues to rely primarily on fossil fuels. This level of investment is also comparable in scale to other recent investments that have transformed the American economy. For example, with advances in unconventional oil and gas production, investment in fossil fuel production has increased to an average of $130 billion per year over the past decade, from less than $30 billion in 2000. An average of $350 billion per year has been invested over the past decade in computers and software, more than tripling the annual investment levels of the early 1990s. These investments have yielded solid returns to those businesses willing to lead.

- These up-front capital investments would bring large reductions in fuel costs, because renewable electricity generation requires little or no fossil fuels, and electric vehicles and other new systems would bring major gains in energy efficiency. The savings would grow from an average of $65 billion per year between 2020 and 2030, to $400 billion per year between 2030 and 2040, and to an average of about $700 billion per year from 2040 to 2050.

- The higher levels of capital investment needed for the clean energy economy would boost manufacturing and construction in the U.S., stimulate innovation, and create new markets. Roughly 460,000 new construction jobs could be created by 2030, with the number rising to 800,000 by 2050. However, dramatically reducing the use of fossil fuels would obviously hurt industries and regions that now depend heavily on coal, oil, and natural gas. It could decrease the number of coal mining and oil- and gas-related jobs by more than 130,000 by 2030 and 270,000 by 2050, with job losses concentrated in the Southern and Mountain states. Transition assistance and job training would be needed to ease these economic dislocations.

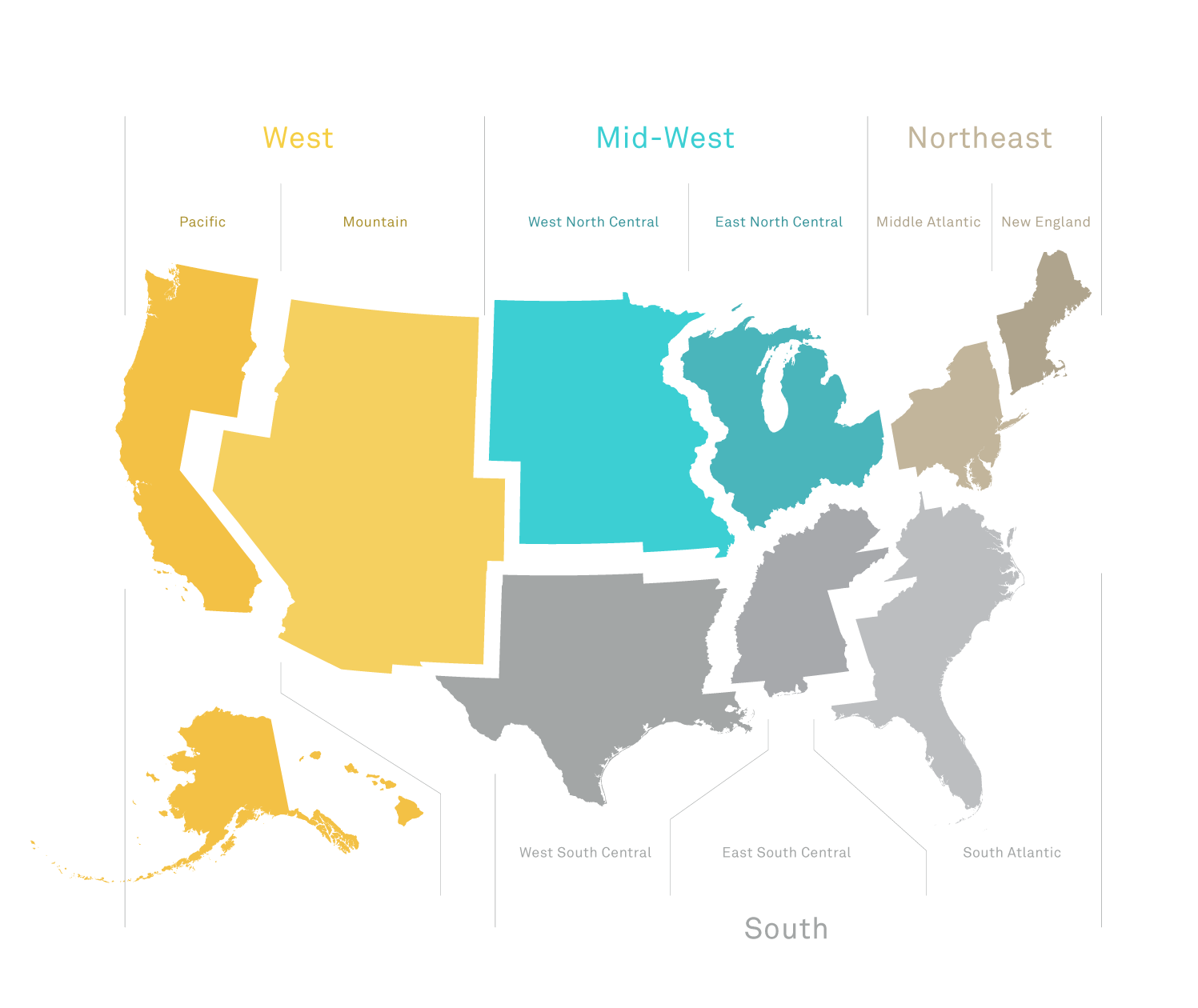

- Because of regional differences in energy consumption and renewable energy resources, each region of the U.S. would see different amounts of job growth and industry gains. Wind power would grow fastest in the windy central region, and investments in solar power would be greatest in the sunny western and southwestern regions. Revenue from biomass feedstocks would be greatest in the Southeast and the Midwest. New nuclear plants would be concentrated in the mid-Atlantic and southern regions, where renewable resources are less abundant and the regulatory framework for vertically integrated utilities is more conducive to such plants.

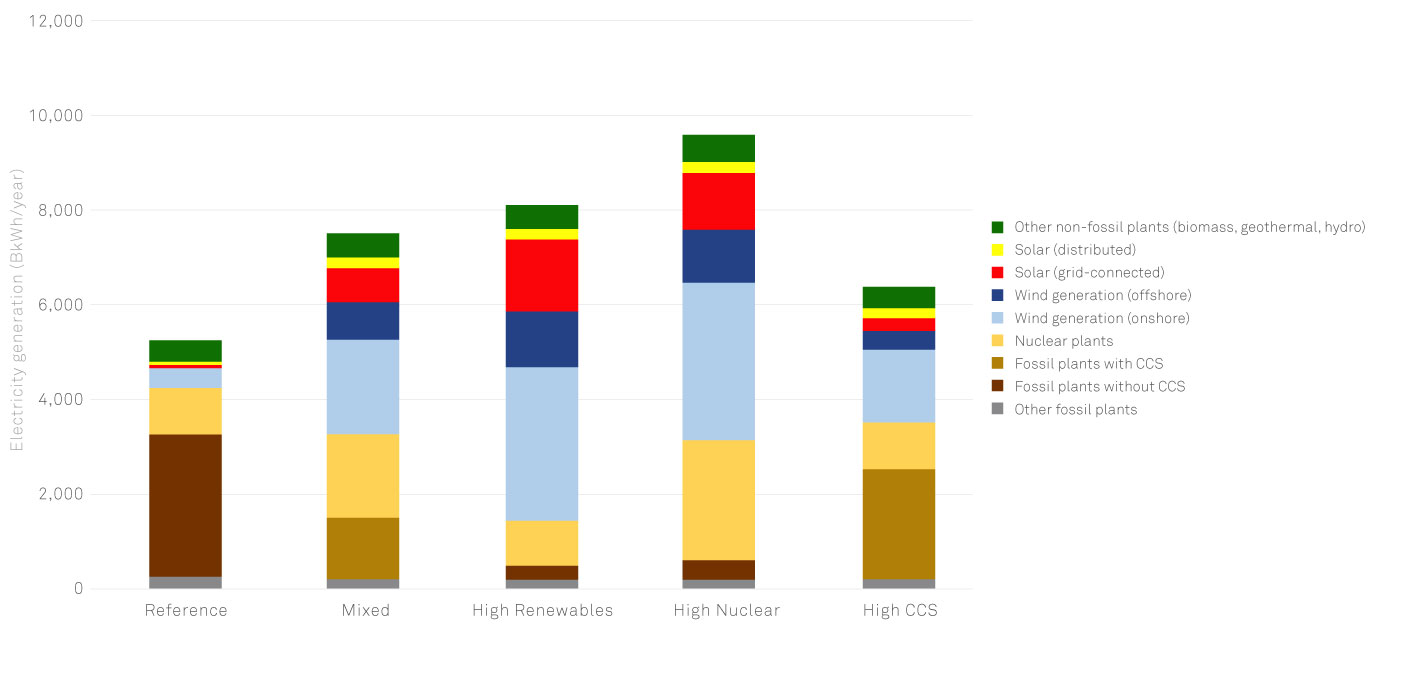

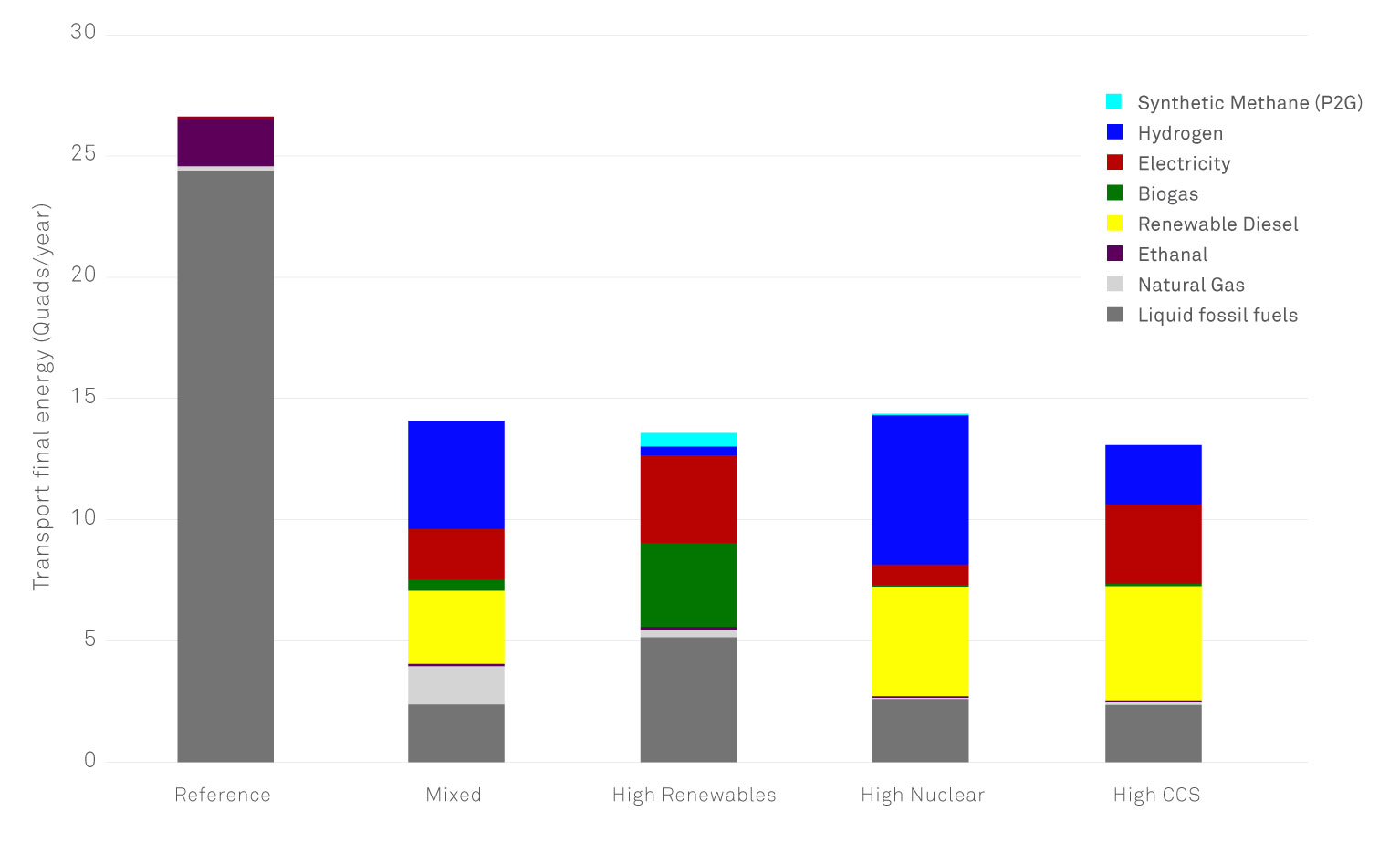

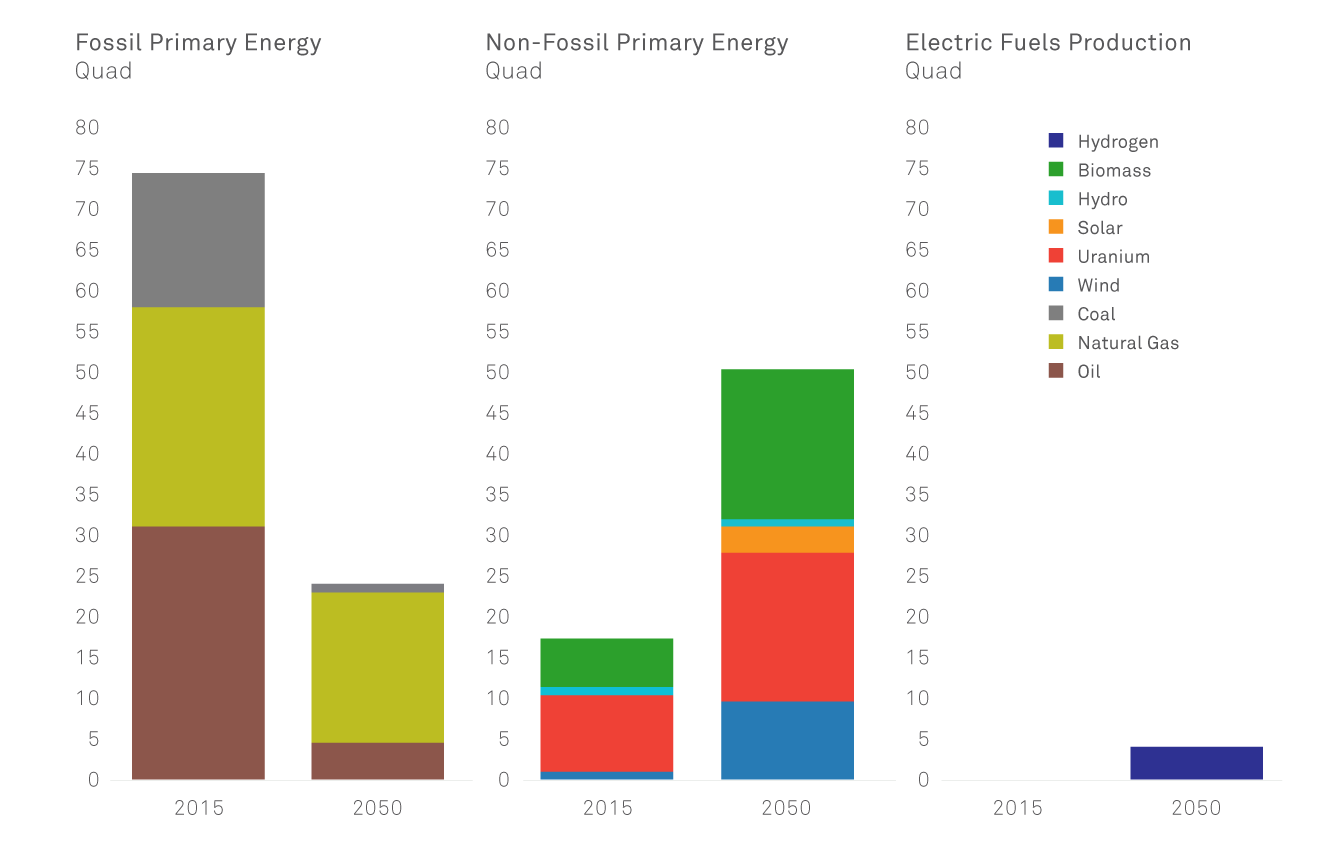

We modeled four distinct pathways that could achieve economy-wide reductions in CO2 emissions of 80 percent below 1990 levels, and compare results to a “business-as-usual” pathway we call the High-Carbon Reference Case. Three of these pathways each rely significantly on one of the three major types of low- and zero-carbon electricity: renewable energy, nuclear power, and fossil fuel power with carbon capture and storage (CCS). The fourth, labeled the “Mixed Resources” pathway, relies on a balanced blend of these three types of clean electricity. Each pathway also includes a different mix of low- and zero-carbon transportation fuels and technologies. We focus primarily in this summary report on the results for the Mixed Resources pathway, but full results are available in the Appendix for the other pathways: High Renewables, High Nuclear, and High CCS. The Appendix also provides additional details on the design of the pathways. The Co-Chairs and the Risk Committee of the Risky Business Project do not endorse any one specific pathway.