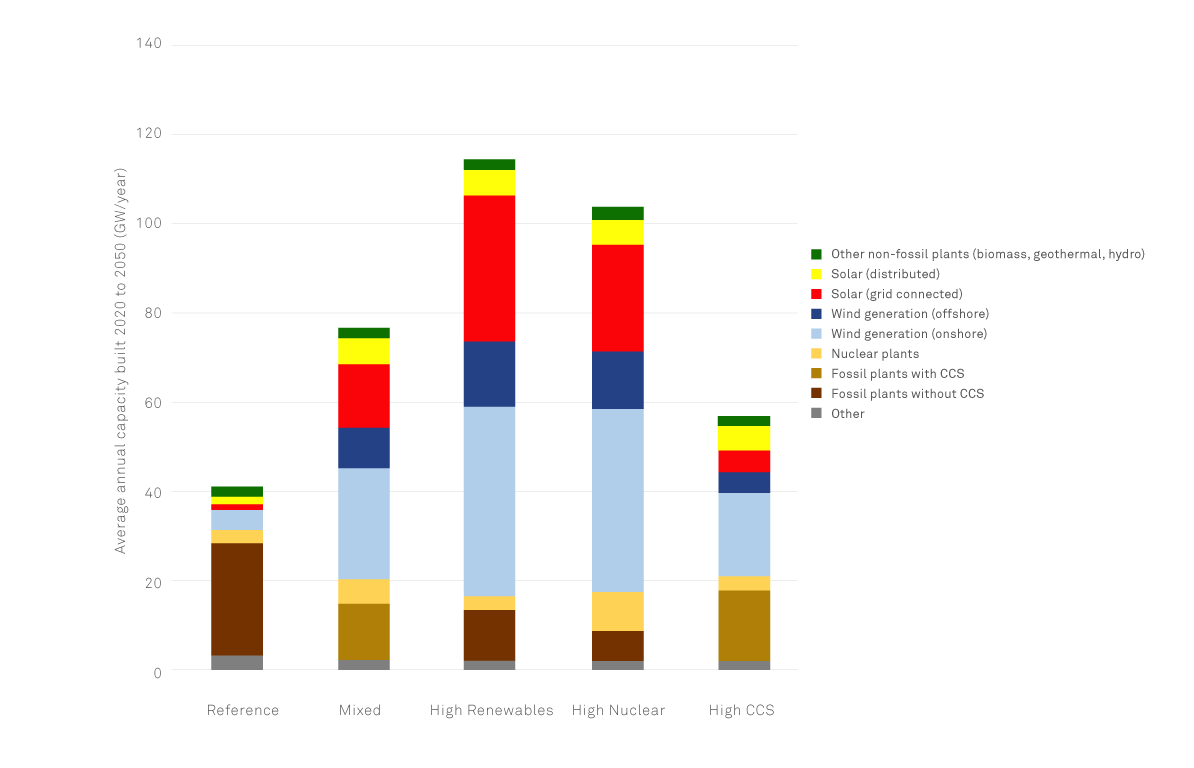

Renewable Integration

The power generated by wind turbines drops when the wind dies. Solar PV output dips during cloudy days and is zero at night. This variability is one of the defining features of renewable power, and requires careful minute-by-minute balancing between load centers and electricity generating units. Yet fossil-fired electricity generating units may have somewhat variable output as well—for example, through forced outages, scheduled maintenance, or transmission constraints on generation—making the integration of variable electricity generation resources not a fundamentally new problem for the utility industry. However, accommodating high levels of renewable power in a clean energy economy would create new operational challenges2 A grid powered with a high percentage of variable renewable energy would have to be highly flexible, and be able to handle variable power outputs on shorter time scales and with less predictability than grids powered largely by fossil fuel and nuclear plants.

Extensive studies of these challenges, and observation of specific states and countries that have moved forward with grid integration plans, make clear that high levels of renewable power can be cost-effectively integrated into the grid without threatening reliability3.

In our PATHWAYS modeling, much of the load balancing is achieved through production of hydrogen and synthetic natural gas4. These facilities would be oversized in production capacity in order to allow them to operate flexibly and absorb excess power generation. However, we expect that to integrate higher levels of renewable generation, grid operators would likely use an array of tools for maintaining the match between supply and demand. In fact, they are already adept at predicting and managing big, rapid changes in load. Tools include dispatchable resources, diverse types of resources, geographic diversity in generation, and the use of energy storage and demand response resources. All of these tools would likely grow in importance as renewable power expands.

A diverse portfolio of wind and solar plants allows for more consistent power supply, as some of the plants can still operate when winds slow or clouds cut solar output in specific locations. Denmark has successfully integrated 39 percent of its total electricity generation from wind power, but its interconnection with Germany has proved critical for balancing periods of surplus or insufficient Danish wind generation5. Renewable sources are best integrated when the grid covers a larger and more diverse geographic footprint6. Building more transmission lines can therefore be important to integrating renewable power on the grid7.

Integrating renewable power on the grid also requires large-scale energy storage8. Parts of California already generate more solar power than can be used during the afternoon on some days9. As a result, California has mandated that utilities add 1.325 GW of storage to the grid by 2020 to capture the excess solar power and to increase flexibility10. Meanwhile, advances in batteries and other storage technologies have caused prices to decline significantly, making them cost-effective for some applications11. Large battery installations in places like Moraine, Ohio, and Elkins, West Virginia, are already being used to manage power quality and short-term fluctuations on regional grids12.

More flexibility can also come from applying information technology to grid operation, creating a “smart grid” which can give customers more ability to match energy use to times when the grid is not already overloaded13. Such technologies will also facilitate the adoption of electric vehicles, allowing the grid to charge these vehicles at times when renewable power is available. Electric vehicles can ultimately serve as a form of energy storage for renewable power, as can space and water heating systems. Ultimately, it should be possible to draw power from connected electric vehicles when needed14, though this technology is still in its infancy.